A Community-Public Banking System can save us tens of thousands of euros in interest payments on every mortgage and would serve the productive economy, and not speculation and boom-bust creation.

The Proposed Comprehensive Public Banking System for Ireland was Presented to Finance Committee 12th Oct 2017:

Presentations on Public Banking begin at 2hrs 27 minutes.

The Tracker Mortgage Scandal is covered before Public Banking.

——————

Pillar Banks or Peoples Banks – Credit Unions & Post Offices hold the key!

PBFI Interview on Limerick Today with Joe Nash –

2022 Plan for Community-Public Banks in Ireland.

Community-Public Banking Ireland – Oct 2022 Plan:

Ireland Urgently Needs Safe, Solvent and Ethical ‘Not-for-private-profit’ Community-Public Banks to provide safety for Irish deposits, support for the Indigenous Economy, and banking facilities to everyone in the country.

As you are aware, Ireland has essentially a banking duopoly with two large international commercial banks holding the vast majority of deposits, accounts, mortgages and loans. This monopoly on lending is essentially control of the ‘credit of the nation’, i.e. they control who gets credit, the purpose for which it can be used and the price of that credit i.e., the interest rates charged. As the vast majority if this lending is for assets and asset speculation, it does not serve the productive economy.

This also contravenes the Constitution of Ireland wherein it states as follows:

“That in what pertains to the control of credit the constant and predominant aim shall be the welfare of the people.”

Bunreacht na hÉireann Control of Credit: Article 45 2(iv),

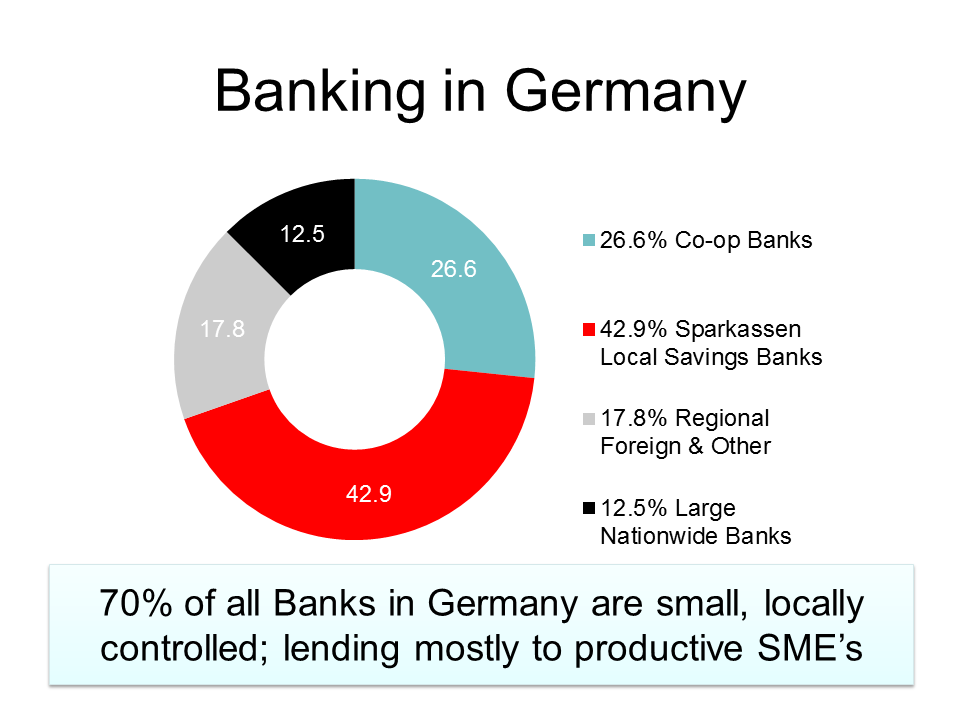

Community-Public Banking System Behind German Economic Success:

Germany has c. 70% Public & Community Banks. The Sparkassen group comprise c. 42% of these, with the remaining c. 28% being Cooperative Banks. All of the Commercial Banks in Germany, including Deutsche Bank and Commerzbank, have only 12.5 % of the market. Germany is the 4th largest economy in the world with exports similar in value to that of China, while having only 6% of China’s population.

Renowned International Banking Professor, Richard Werner, describes the current scenario very simply:

“Economic Growth and National Income are almost entirely determined by a factor that is decided at home (in Ireland), namely, the amount of bank credit created for productive purposes.”

Professor Richard Werner

Ireland needs,

1. Banks Providing Safety from bail-ins for Irish deposits.

2. Banks based on systems proven to work and create strong, high growth economies, e.g. Germany, Japan, Korea & China.

3. Banks offering Community Control of Credit (SME Focused Banks – SME’s provide 60 to 70% of all jobs)

4. Banks facilitating ‘Credit for Productive Purposes’, i.e. to create new jobs and services.

5. Banks that Do Not participate in Securitisation or Speculation, and do not pay Banker Bonuses.

6. Banks that counter the ‘Boom-Bust cycles’ created by speculative credit of commercial banks.

7. Banks that Retain ‘Physical Cash’ in society as the commercial banks and ECB now work to remove it.

8. Banks that remove ‘Control of the Credit of the Nation’ (i.e. the economy) from private Banks.

9. Banks that are Decentralised – Reverse the globalists trend of Centralisation.

We can have local jobs, rural and urban revival and development, with ethical Community-Public Banking.

No Government/State Support – The Project Must Proceed

As no Government/State support is forthcoming for the 2015 SBFIC – Sparkassen/PBFI proposal for eight to ten Regional Community-Public Banks, or for the PBFIs 2017 Preliminary Proposal ‘Creating Ireland’s Alternative Banking Force’, the PBFI together with ‘Local First Initiative’, a not-for-profit CLG and other groups, together with public support are proceeding with an initial modest proposal of two Regional Community-Public Banks and a Central Support Unit (CSU) for the 26 counties, as shown in the graphic above.

Local First Initiative is a not-for-profit CLG, setup to support community benefit projects.

Note: Northern Mutual an independent group in NI have begun a Community Banking project in the 6 counties.

The CSU will be required as more banks are added to the network later. A Comprehensive Nationwide Community-Public System is required; ideally a Community-Public bank in most every county, with smaller adjacent counties grouped to makeup the required population.

The graphic above shows the Three Regions.

Community Banking in Bavaria

Funding:

For a total Once-Off cost of c. €30M (c. €6 per man, woman and child in Ireland) we can have Two New Ethical, Solvent and Safe Regional Community-Public Banks.

Funding will be raised by the following methods,

- Membership fees & pledges (An Irish address, within the 26 counties is required).

- Crowd Funding.

- Donations.

- Grants.

- Funds from other fund raising initiatives.

A Comprehensive Regional Community-Public Banking system is needed in Ireland to drive our indigenous economy and rural revival and as a safe place for Irish deposits and savings.

Circa. €83k could be saved on every average mortgage in Ireland.

Sept 2022 Example.

Average House Price Ireland Mid 2022 €294k –

Mortgage: 90% LTV (Loan to Value) – Borrowing €265,917 – 30 Year term

Fixed for 10 Years

Interest Rate in Ireland 2.85%*

Total Interest Ireland €129,493*

Interest Rate in Germany 1.1%

Total interest Germany Community-Public Bank €46,213.

Saving in Germany of €83k over life of Mortgage.

*Best Rate Ireland Sept 2022 CCPC.ie; 2.85% (Initial interest rate) https://www.ccpc.ie/consumers/money-tools/mortgage-comparisons/ Indicative APRC for full term not applied to either mortgage.

Circa. €83k COULD BE SAVED ON EVERY AVERAGE MORTGAGE IN IRELAND!

Banking Models like the 70% Community-Public Banking Model in Germany has enormous benefits for people, communities and the country in general.

It is ‘Banking in the Public Interest’

Record Your Support for the Project.

E-mail admin@publicbankingalliance.ie

Germany has almost 70% Public & Community Banks;

It has 42% Sparkassen Public Savings Banks (Est. 1778) comprising ~400 Independent Public Banks with 15,000 branches and 26% Cooperative Banks, comprised of 1,050 Banks.

- They are the backbone of the successful German economy; the fourth biggest in the world.

- They serve the community and prioritise lending to small and medium size local businesses.

- They are regionally bound and regionally focused and prioritise the prosperity of their region.

The Private Commercial Banks in Germany have only 12.5% of the market.

Prof. Richard Werner Conference – Banking Industry Exposed & Solutions Presented – Dublin April 2016

‘Creating Ireland’s Alternative Banking Force’

Incorporating the Credit Unions & Post Office Network.

Tommy Marren Interviews Seamus Maye, Joint Chairman & Spokesman for the Public Banking Forum of Ireland (PBFI) on the PBFIs Preliminary Proposal ‘Creating Ireland’s Alternative Banking Force’

————–

Financial Institutions that Serve the Real Economy.

Dr Thomas Keidel & Christopher Simpson (CIVITAS)

German Savings Banks Association

The German Model

SPARKASSEN

The German Public Banking Model – Two centuries of dependable dedicated service.

The German Savings Banks, the Sparkassen (Meaning Treasure Chest) Founded 1778, has 42% of the total German market and provide 42.7 per cent of all finance to German businesses.

The Sparkassen dependable support of German Mittelstand (primarily small and medium firms SMEs) is the backbone of the German economy. Some 86% of German businesses have an annual turnover of less than €1m.

These banks increased lending to SME’s by 17% between 2008 and 2011.

The German Public Savings Banks have

- 42% of the overall market in Germany with 50 million customers;

- 75% of the SME Start-up market.

- 30% of the Farm lending market.

The German financial system is comprised of

c. 70% Public Banks – 42% Sparkassen Public Savings Banks & 26% Co-op Banks.

The Private Commercial Banks have only 12.5% of the Market.

German Public Savings Banks:

- Operate on commercial principles with the aim of maximising sustainable lending as

opposed to maximising profits, bonuses and shareholder returns. - Operate on the Principle of “Local deposits into local loans” keeping capital in their own

area. - Their Public Mandate guides them to maximise the competitiveness of their

region. - Their dependability and financial performance is well proven over many

decades. - Surpluses remain with the bank & within the region. Profits are used to increase equity

and for non-profit social purposes (the public benefit principle). - Prudent self-regulation and their public mandate prohibits engaging financial

speculation & securitisation. - They are permitted to lend only to local people and businesses in its designated area.

- Controlled by community stakeholders and a professional bank management team.

Germany also has over 26% Cooperative Banks:

Financial Crisis of 2008 a Boost for Sparkassen German Public Savings Banks – Funds came rushing in to safety.

In 2008 when the European private bank failure was unleashed on the public,

- €1bn in deposits came rushing in to the safety of the German Sparkassen Public Savings Banks in just a two week period.

- No Public Savings Bank required a bail-out in the crisis.

- The Public Savings Banks actually increased lending to SMEs/businesses by 17% between 2009 and 2011; much of the new funding went into R&D as product demand dropped because of the crisis.

Germany Vs Ireland in Banking

- Germany has only 12.5% Private Banks;

- Ireland has close to 95%

- Irish Credit Union funds are by law held in the Private Commercial Banks. (Estimated at €7bn; are they safe – are they still there?)

No safe place for deposits in Ireland

- Deposits up to €100k Guaranteed by a broke indebted Government. (Any issues; we the taxpayer will pay)

- The private banks have the guarantee of a bail-in when they need rescuing next time. (EU law since 2012)

Shouldn’t we have a safe haven for our deposits for when the Bail-in’s that have started in Europe come to Ireland?

PBFI 2017 Proposal Creating Ireland’s Alternative Banking Force

Preliminary Proposal by the PBFI.

Creating Ireland’s Alternative Banking Force –

Incorporating the Credit Unions & the Post Office Network:

Published March 2017

Link to full screen version of ‘Creating Ireland’s Alternative Banking Force’ Here